Overview

Richwood Bancshares/Richwood Bank has been in business since 1867 and is focused on providing shareholders new ownership options and continually attracting new investors.

The bank’s leadership wanted to ensure that existing shareholders and customers had an opportunity to either increase their existing stock ownership or become new shareholders. They also wanted to provide new investors with the opportunity to become shareholders of Richwood Bancshares, the parent company of Richwood Bank. Utilizing a self-directed IRA program to support a public stock offering allowed the bank to attract local, long-term investors; and by providing shareholders with a program in which to use the historically long-term investment dollars of IRAs for investing in bank stock.

Key Issues

Richwood Bancshares/Richwood Bank saw the benefit of matching long-term investment dollars (typically kept in IRAs) with the historic long-term hold of community bank stock. The bank’s shareholders, directors, and executive management had previously utilized the capability offered by various brokerage firms to place their existing Richwood Bank common shares in these firms’ respective self-directed IRA accounts which,in many cases, provided a beneficial service to existing shareholders. However, this strategy also created unexpected consequences:

- Brokerage firms charged account maintenance fees to account holders.

- Dividends paid to shareholders must go through DTC in order to be deposited, subjecting the bank to the added cost of FINRA fees.

- Brokerage firms could not readily sell the securities because they were privately held.

- Brokerage firms can place a trading symbol on the company … the first step in becoming a publicly traded stock

- Privately-held stock can be difficult for brokerage firms to place in, or remove from, a self-directed IRA. For example, a distribution or transfer typically takes several weeks.

The Solution: Create Self-directed IRA Capability That Also Supports a Secondary Offering

It was important to Richwood Bank that a planned stock offering was expeditious and demonstrated to investors high interest and value. However, the bank was not aware of any banks in their market area that had included a self-directed IRA program as part of their product offering and sought the guidance of CAMELS Consulting Group which has extensive experience in the implementation of self-directed IRA programs in the community bank sector. The implementation included:

- A shareholder accounting function to handle the record-keeping and either certificate preparation or book entry through CAMELS’ recommended price-competitive software system, StockTrack.

- The multitude of operational and compliance processes for setting up a self-directed IRA.

- The establishment of policies and processes with specific guidance from CAMELS Consulting Group on handling the purchasing, distribution and selling of the bank’s shares through a self-directed IRA.

- CAMELS Stock Valuation Program to establish the fair market value on the stock for all shareholders and to regularly communicate the stock price through year-end reporting and periodically throughout the year establishing fair market value on stock transactions, an important element for instituting a self-directed IRA program.

CAMELS Delivers Results

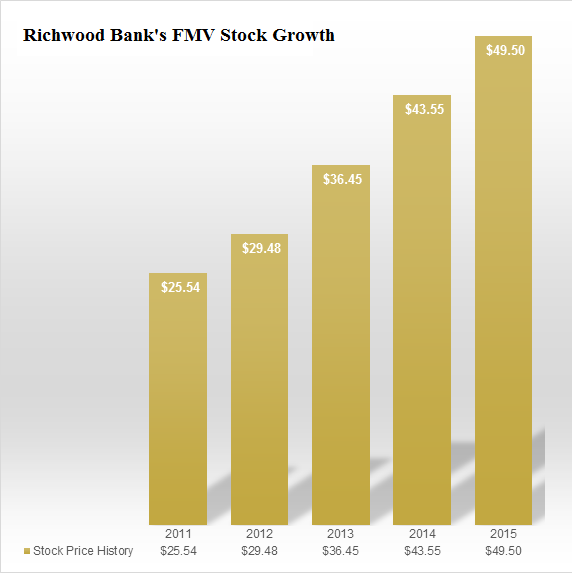

After the implementation of CAMELS Self-Directed IRA Program, Richwood Bank’s stock ownership grew significantly and its liquidity was greatly enhanced, providing a natural outlet for the purchase of stock by self-directed IRA account holders. In addition, CAMELS Consulting Group helped set up the bank’s self-directed IRA account holders for additional purchases in subsequent years as they contribute to their IRA.

Specifically, Richwood Bank’s self-directed IRA program is an important element in supporting shareholder liquidity. Today, Richwood has approximately 1.3 million shares outstanding and continues to market its self-directed IRA program realizing ongoing growth in new shareholder ownership and the concurrent ability to handle large block transactions.